A site for recollection and reemphasis of entrepreneurship and sound business practice. A compilation of both theory and practice of business entrepreneurship. The author is both a practicing businessman and former academic

Every generation needs a revolution - an entrepreneurial revolution

Credit Suisse Bank is facing huge losses due to its handling of risky assets. Is laying off staff, shares prices decline. Bad banking decision. And the contagion could spread in Europe It is hobbled by its involved in bankrupt Greensil and British financier Greensil (also linked to another Indian billionaire)

Banks worldwide are undercapitalized and could wobble There were posts that some banks could go under with estimates that worldwide the capital is a little only $100B with high estimates of $1.7 trillion. mainly due to the revaluation of asset quality. These are uncertain times Even venerable banks are not exempt from the crisis and instability

For banks in US, due to covid and inflation, the $2 trillion or so savings of Americans could evaporate as citizens cope up with inflation (diminished spending power) and liquidity in banks could evaporate

Sri Lanka (the home of Tamil Tigers) was the first. Second is Pakistan A well developed country with large population It has ran out of gas, and currency to import its basic necessity.

Why does a country go bankrupt?

1. Lack of revenues; poor ways and means and tax collection;

2. Diminished exports

3. Too much dependence on imported products.

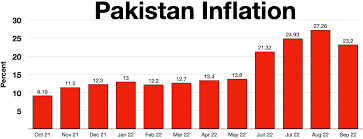

Bad weather and faltering exports have not been kind to Pakistan economy Dollar reserves stand below $5 billion, its worst. (compare this to PHL below $100 billion) Banks have refused to extend LC for its imports (Can it still rattle saber with India?)

It is still in difficult negotiation with IMF for a $6B bail outs. The top guys of the country must have rubbed the IMF guys for alleging that the conditionalities included non nuclear stance of the country ( could be Why do we lend to a country who could be using the funds to fuel a future of the war, that could endanger the world) I does not get too the usual cash assistance from KSA who as fellow Islam country is ready to lend on a phone call The KSA head impose conditionalities like strict revenue imposition, and financia controls, just like the IMF

Every generation needs a revolution - an entrepreneurial revolution

This post was banker for a while and is a student of investment banking, especially how the same helps in nation building. The more important thing is have we learned from this.? It has been a decade and a half since the crisis and it seems we are facing another one, albeit from a different cause (covid 19)

For 2008 many experts believed that other causes were the

1. bonus system that rewarded more sales irrespective of the risks

2 the lack of supervision and control in a deregulated environment (the head of the Treasury was former head of another IB - Goldman Sach

Central to the crisis of September 2008 was the subprime mortgages

1. Bankers from all over thought that the Treasuries were too low and therefore went into mortgage backed securities. They gave higher yield than Treasuries The Mortgage Backed Security were nothing more than pool of mortgages packaged and sold as securities. and were sold from bank to bank. No one seemed to shoulder the responsibility or risk for the securities, which was present if the loan was underwritten by the bank alone and held into.

At that time real estate was booming in USA, and everybody across the world wanted a piece of that boom at least for MBS. If the borrower defaults, the house could still be sold at a profit.

2. There were prime and subprime mortgages The prime were good mortgages that passed the standards of poor credit (This post experienced this with instruction of going by formula lending, ie

Amount of monthly loan eligibility x 36 = loanable amount.) The credit worthiness and scoring went down to the gutter

3. Subprime mortgages were below par as per credit standards. These were housing to loans to people

who can ill afford to live within their means much less pay the normal amortization. The mortgage companies engaged in predatory lending ie that loans were offered with little amortization in the beginning to lure them into borrowing; But a year later the payments would balloon. The borrowers cannot afford and then default

The house would be foreclosed and cant be resold No one wants to buy the foreclosed house (or if the

neighborhood did not look prime)

4 These result in more defaults and the MBS became worthless or in the term of the IB toxic

5. First to notice this was BNP (Paribas) in Paris And soon the toxicity spread across Europe and the world. Eventually ending up with Lehman brothers who had large exposure.

We also note that some IB kept on selling securities back in forth to generate more turn over, (sales) and commission for the brokers traders At some point Lehman sold to Cayman banks (on a repo) MBS

worth almost $100 billion. Note this was not a borrowing but a sales (the repo tells you it is a borrowing). So no civil or criminal cases can be filed

The head of investigating team that held the hearings say that some products can be toxic over time And that is fine but not with sub prime mortgage which was toxic from the very start And no one, no one seems to bear responsibility to the quality of the toxic product: not the underwriter, or the packager, not the rating agency, not the auditor (if any) No one No one seems to care

May be we asked for it

The debacle caused loss of jobs for nearly 30,000,000 Americans, not to mention loss of money, loss of confidence in banking system and very harsh lesson for top execs of Lehman and other banks worldwide. Did we learn our lessons?